")

")

Amid deep market volatility this year, few companies have elected to go public, and fewer still have turned out to be success stories. Still – investors that are willing to be patient and time their purchases correctly can have the opportunity to earn outsized gains.

Reddit (NYSE:RDDT) is an incredibly interesting new IPO. The social media company insists on being differentiated from its crowded industry by emphasizing its focus on communities and common interests. Whereas Instagram (META) and TikTok are more for showcasing your own content, Reddit encourages discussions and chat rooms based on topics of commonality.

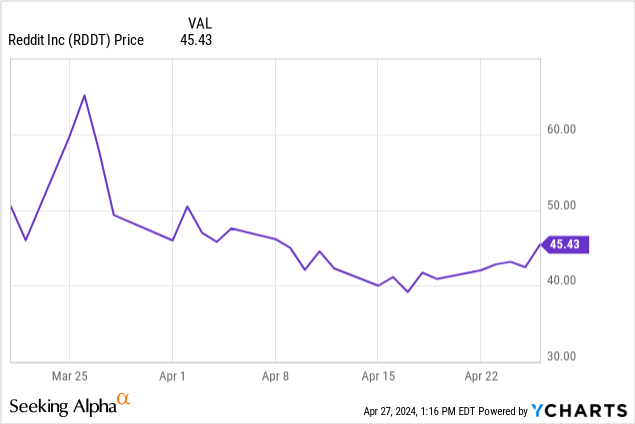

Reddit priced its IPO in March at $34 per share. It initially surged as many tech IPOs do and briefly crossed $60. Now the stock has settled in the mid-$40s, creating a more normalized environment for potential entry.

To cut to the chase: I’m initiating Reddit with a bullish rating and I am looking for an entry point amid the post-IPO dip. Here are the reasons why.

Reddit versus peers; a growing user base

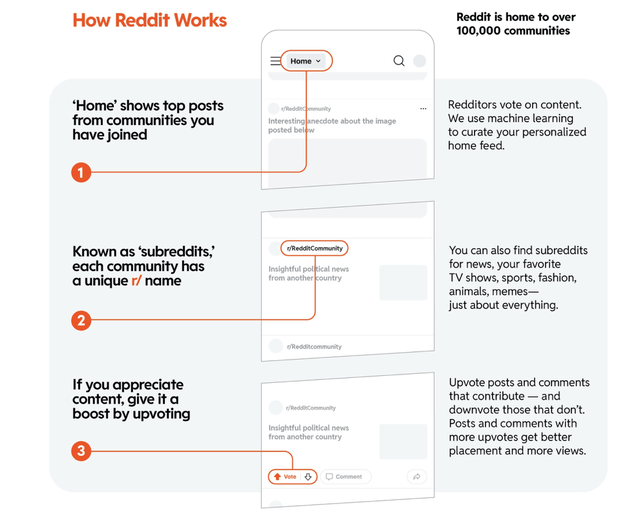

Reddit is focused on distinguishing its platform as a community of like-minded individuals who engage in helpful discussions. Whereas other social media platforms are more for self-promotion (which, as many observers have pointed out, can be damaging for self-esteem, especially among comparison-minded young adults), Reddit has a unique system of “subreddits” that are centered around community-based interests.

How Reddit Works (Reddit prospectus)

The chart above, taken from Reddit’s finalized IPO prospectus, gives a general overview of how the platform works for people new to the concept. Reddit also touts a unique system of “upvotes” and “downvotes” wherein users can signal their approval or disapproval of other users’ messages based on how helpful they were to contributing to a particular discussion.

Reddit users also accumulate a system of points called “karma” – which is their net tally of upvotes and downvotes – that can be publicly seen on their profiles. The higher a user’s karma, the more trustworthy that person’s commentary is viewed as being.

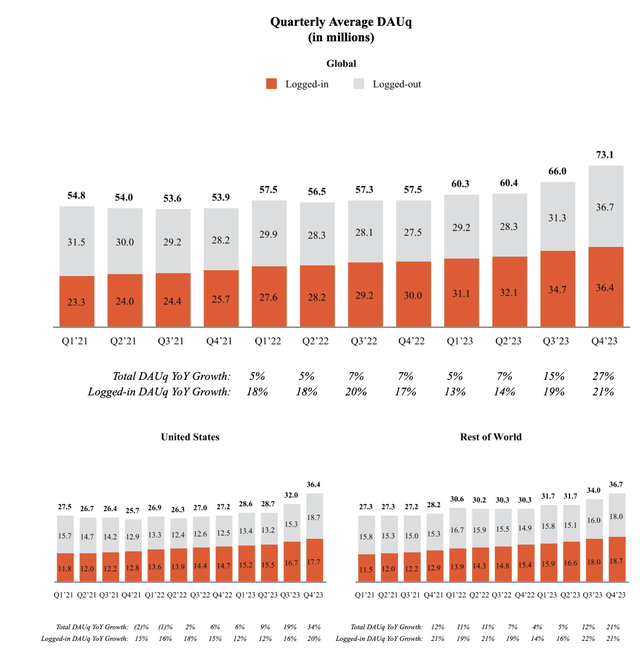

Reddit, arguably, is a much smaller social media platform than many of its competitors. As of its most recently reported quarter (the December 2023 quarter), it counted ~73 million DAUs (daily active users).

Reddit DAUs (Reddit prospectus)

Meta (META), the largest social media company, has more than 2 billion DAUs, while Snap (SNAP) has over 400 million. I’d argue the closest comparison to Reddit is actually Pinterest (PINS), where communities also form around topics of interest (but as a platform, Pinterest is more focused on images and links to websites to purchase items; whereas Reddit is more text-heavy and discussion-based). Pinterest does not report DAUs, but its MAU (monthly active user) count as of its most recent quarter is just shy of 500 million.

Where Reddit earns my respect as an investor versus other social media companies: Reddit is growing U.S. users substantially, whereas many of its competitors have reached a saturation point in the U.S. This is so critical because U.S. users have substantially higher ARPU (average revenue per user) than international users. The fact that Reddit added 3.4 million U.S. DAUs (+34% y/y) in its most recent quarter is an incredible lever for growth and monetization.

Revenue model

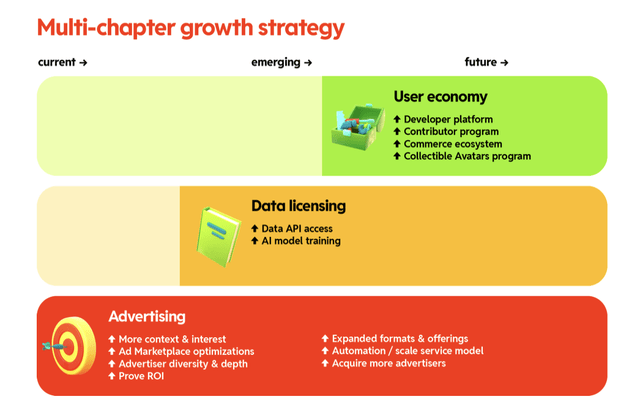

Like all social media companies, Reddit generates the lion’s share of its revenue from selling advertising space. Yet in recent years, the company has also opened up two new paths to monetization through data licensing and user e-commerce:

Reddit monetization pillars (Reddit prospectus)

In particular, I think the data licensing element of Reddit will be a key growth driver in the future. Reddit generates heaps of valuable, easily ingestible text data from all of its user-generated content. It already sells this data (anonymously) to third parties as a way of training large language models (LLMs). As more and more applications are built on LLMs and AI proliferates more and more into everyday functions, Reddit’s data licensing strategy can offer a powerful recurring subscription revenue stream for the company that has endless use cases for customers.

Reddit’s marketplace business is an interesting play, but in my view outclassed by Pinterest – which is the larger platform and more oriented toward physical goods. The company notes in its prospectus that ever since launching in June 2022, the company has signed up more than 30 million active connected wallets. There is potential here for transactions of digital goods, as Reddit does provide a developer platform (where, for example, like-minded users can gather and sell originally developed video games). Overall, however, I view data licensing to be the more attractive longer-term tertiary revenue opportunity.

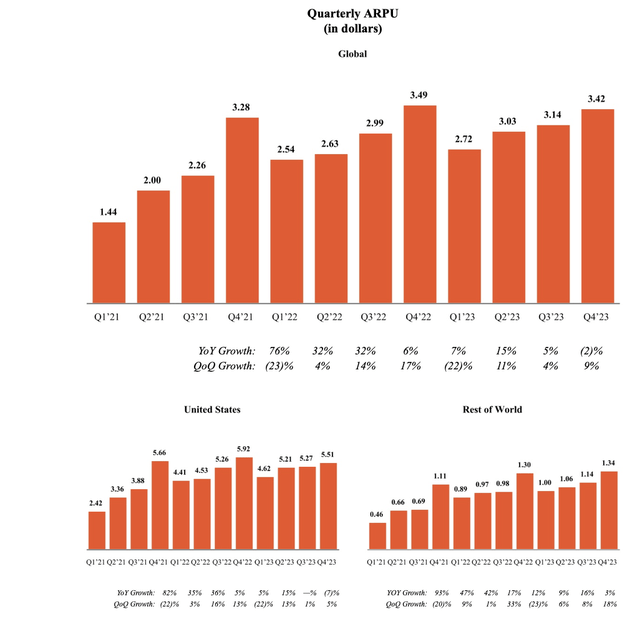

Reddit’s ARPU has stabilized in the ~$3 range. ARPU did decline -2% y/y in the most recent quarter, notably in the U.S.

Reddit ARPU (Reddit prospectus)

However, outsized U.S. user growth (and the fact that the U.S. generates ~4x the ARPU of an international user) should help to boost ARPUs over time, plus with additional revenue opportunities from non-advertising helping overall platform monetization.

Financials and valuation

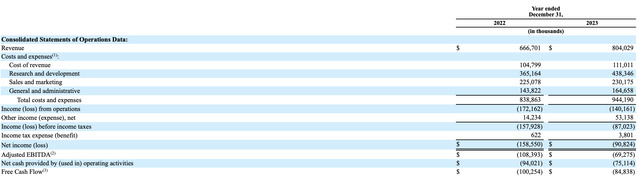

In short: Reddit is still growing double digits, but not yet quite profitable.

Reddit financials (Reddit prospectus)

It grew revenue at a 21% y/y pace in FY23 to $804 million. Growth did accelerate in the fourth quarter of FY23 to 25% y/y growth, driven by a sharp jump in its U.S. user base.

To date, Reddit is still losing money: though adjusted EBITDA in FY23 showed a -37% y/y smaller loss at $69.3 million, or a near-breakeven -9% adjusted EBITDA margin. The great news here is that Reddit has high GAAP gross margins at 86% in FY23 (taking out $111 million in cost of revenue), which means that its 20%+ growth flows almost entirely to the bottom line. At present, Reddit is spending more than half of its revenue on R&D as it has released a plethora of new features over the past couple of years (including its marketplace features). Over time, the company should be able to scale nicely on opex.

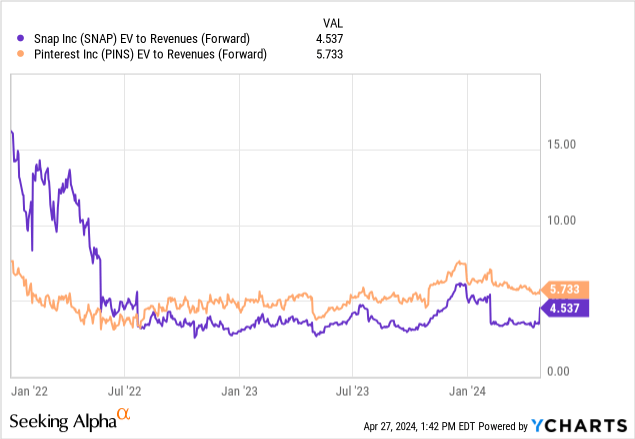

From a valuation standpoint: at current share prices near $45, Reddit trades at a market cap of $7.37 billion. After we net off the $1.21 billion of cash on its December balance sheet, as well as the $473 million of net IPO proceeds it reported in its final prospectus, we arrive at an enterprise value of $5.69 billion.

Meanwhile, consensus is expecting Reddit to generate $986.0 million in revenue in FY24, or 23% y/y growth; and $1.21 billion (+23% y/y again) in FY25.

This puts Reddit’s valuation multiples at:

- 5.8x EV/FY24 revenue

- 4.7x EV/FY25 revenue

This is roughly in line with both Pinterest (which is achieving ~10% y/y revenue growth) and Snap (which grew ~20% y/y in its most recent quarter, but has lumpier history).

While I don’t necessarily think Reddit is undervalued relative to its peers, I do think the company’s relatively unique platform identity, its high gross margins, its potential in data licensing, and most of all its outsized U.S. user growth afford a premium for the company. My price target on Reddit is $55, representing ~20% upside from current levels and 6x EV/FY25 revenue.

Key takeaways

In my view, after falling ~30% from post-IPO heights, Reddit is worth a buy. My bullish outlook hinges on whether its user growth, especially in the U.S., can be sustained (competition and saturation is one of the core risks for both Reddit as well as the social media industry at large), but so far, I see more opportunity than risk in this stock at current levels.

Read the full article here

Q1 2024 Earnings Call Transcript")

")