(NYSEARCA:SGOV)")

Introduction

Recently, I have been writing a lot about macroeconomics. This has always been an area of study for me, but shifting my attention away from exchange-traded products (“ETP/s”) has changed my outlook on products I have previously recommended, like the iShares 0-3 Month Treasury Bond ETF (NYSEARCA:SGOV).

For those who are not regular readers of mine, SGOV has been one of the very few securities to get multiple “strong buy” recommendations from me.

This story starts back in October 2023, where I wrote about the inverted yield curve making T-Bills the best investment for conservative investors and those wanting to park cash, “Standing Atop the Yield Cliff.”

I put my money where my mouth is, and I have been holding my cash partly in SGOV since December. You can read the first article here, and the second one here, if you want to see my thoughts on SGOV in the past.

I’ve linked all of that to demonstrate that this decision to downgrade SGOV, which I believe will earn me some flak in the comments section, does not come lightly and falls on the back of several months of discussion around this product and its role in modern income portfolios.

This downgrade is from a “strong buy” to a “buy,” as I see T-Bills offering suboptimal yields moving forward compared to other products. CDs, specifically brokered CDs, carry less risk and are now offering yields that are not only comparable, but exceed what we can expect T-Bills to offer this year and next.

The Fed

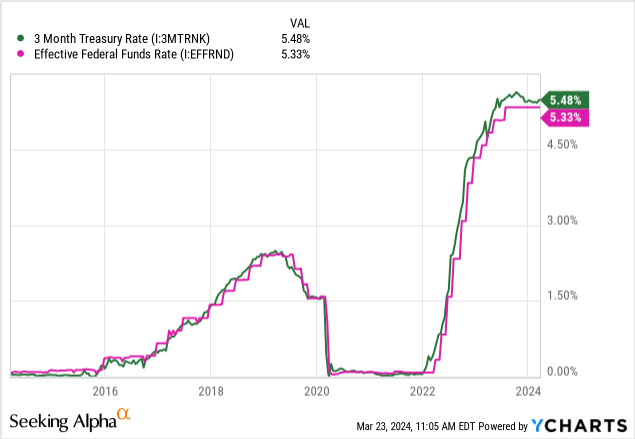

It’s easy to just point a finger at the Fed, since the Fed Funds Rate directly impacts the T-Bill yield. There is no denying that for T-Bill investors, following the macroeconomic picture of the US is important, since the Fed’s decisions on rates change the yield of these products dramatically.

SGOV, being entirely a basket of T-Bills, directly derives its yield from that rate as well. This means that its yield is expected to fall alongside the Fed Funds rate, which is set to see at least three rate cuts by the end of the year, according to the Fed.

This is not set in stone, and the “higher for longer” narrative resurfacing is a risk to consider, but the Fed usually does not like to speculate about rates and prefers to be more direct.

Three rate cuts will leave the Fed funds rate from its current rate of 5.25% – 5.5% down to 4.5% – 4.75%.

By December, SGOV’s yield will likely fall to around that rate, shaving off a 100bps from investor returns.

Locking In Your Rate

So what’s the alternative for conservative investors that have been using SGOV for a cash holding?

My take: build a ladder of CDs that should exceed the expected Fed Funds Rate.

In the long run, these will end up paying more than SGOV as their rates are fixed and SGOV’s is variable. The bonds inside SGOV are fixed rates, but because the fund has to turn over bonds and buy new issues, they will buy them at the lower future rates.

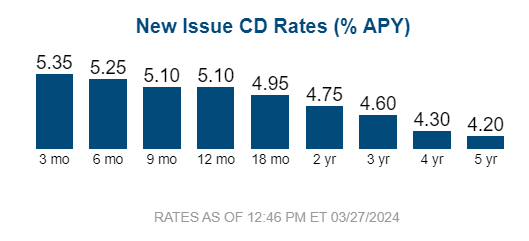

There are some good options to lock in these higher rates for a longer time than SGOV is going to be offering them (so long as we believe the Fed).

Figure 1 (Fidelity Investments) Figure 2 (Vanguard Group)

Currently, investors are able to lock in 5.15% for three years, which is incredible considering that will likely be far above the Fed Funds Rate in 2027.

Projections

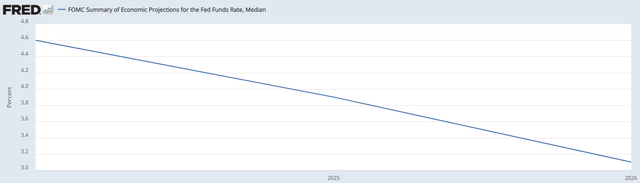

The Fed only projects as far as 2026, but they are projecting to be down to 3% – 3.25% by then.

Figure 3 (FRED)

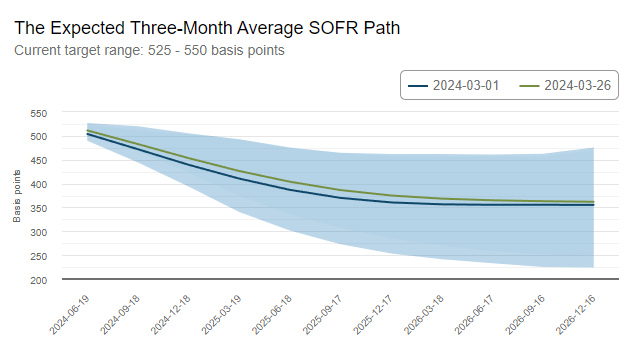

The market also seems to believe this narrative, with the futures market seeing 100bp rate drop in a year’s time.

Figure 4 (Federal Reserve Bank of Atlanta)

The olive line in Figure 4 shows the most recent projections, tightening up since before the FOMC minutes released this month.

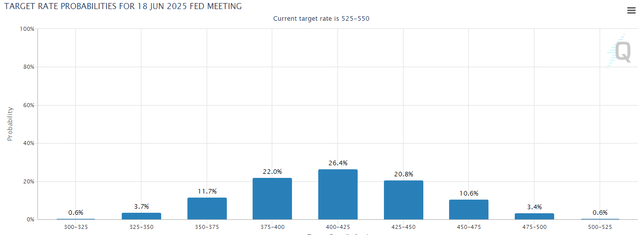

Consensus is that we will not be at the same rate by the end of Q2 2025, with the market predicting an almost 70% chance that we will be within 3.75% – 4.5% by then.

Figure 5 (CME Group)

This means that SGOV’s yield, in a year, will likely be within that range.

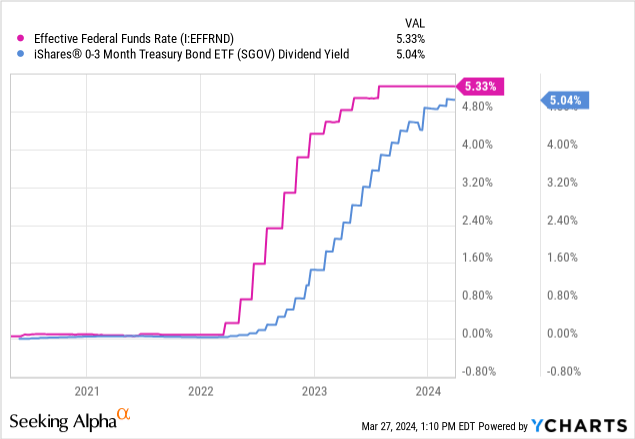

We can see that SGOV’s yield directly follows this rate with its own yield, albeit with a big of lag since the new rates don’t take into effect into the fund rolls its bonds over.

This is not the case for CDs, which pay static yields for their duration.

So if I were wanting the highest yield on my cash for the next few years, I have two options:

- SGOV, which has a current yield of 5.35% but will likely have a yield of <4.5% in a year, and <3.5% in two years

- Brokered CDs, which have a current yield of 5.15%, but will have a yield of 5.15% in both a year and two years

On the back of this logic, I find it prudent to downgrade SGOV to a “buy” as it now not the best in class option for conservative investments like cash holdings.

Certificates of Deposit

Finding the best CDs can be tough, since it really depends on what investors have access to. Certain brokerages will allow you to buy CDs through them, which is what I recommend over buying them via banks. This is due to the extra liquidity given to brokered CDs, since they can be sold to the secondary market more easily.

Fidelity’s list of CD yields can be found here.

Vanguard’s list can be found here.

Risks

There is a risk of the rates going up after you lock in a long-term CD. Being stuck with a lower yield than T-Bills can be detrimental to long-term returns and the ability to keep up with inflation.

There is also a risk of not being able to roll earlier CDs into similar rates. If you lock in a 3yr CD now, you’ll be beholden to the going rate in 2027 for your re-investment. By then, we may be back down around 2% – 2.25% (if we believe the Fed), meaning you won’t be able to re-invest at the 5.15% rate Vanguard is currently offering.

Reinvestment risk is a minor concern, at least, since CDs typically have no potential for loss so long as you hold to maturity. This is also mostly true of SGOV, whose price fluctuates in a predictable pattern and rarely changes much since duration is so low.

Conclusion

It is now becoming more favorable to buy CDs over T-Bill ETFs like SGOV, since they will be slowly lowering their rates alongside the Fed this year. As this happens, investors in SGOV will see smaller and smaller dividends in line with the falling Fed Funds Rate while CD investors will be able to lock in a fixed rate, potentially outperforming the Fed Funds Rate and T-Bills moving forward.

I am currently dropping the iShares 0-3 Month Treasury Bond ETF to a “buy” from a “strong buy” as there is a clearly better alternative in brokered CDs offering upwards of 5% for the next few years. Particularly, Vanguard’s 3yr CD at 5.15% looks incredibly attractive for cash savings.

This downgrade does not mean that I am offloading SGOV. Instead, I am redirecting new cash being added to my portfolio into CDs. When the first rate cuts happen, I will re-evaluate my position on SGOV again.

Thanks for reading.

Read the full article here

Q1 2024 Earnings Call Transcript")

")