The Weekly Closed-End Fund Roundup will be put out at the start of each week to summarize recent price movements in closed-end fund [CEF] sectors in the last week, as well as to highlight recently concluded or upcoming corporate actions on CEFs, such as tender offers. Data is taken from the close of March 15th, 2024.

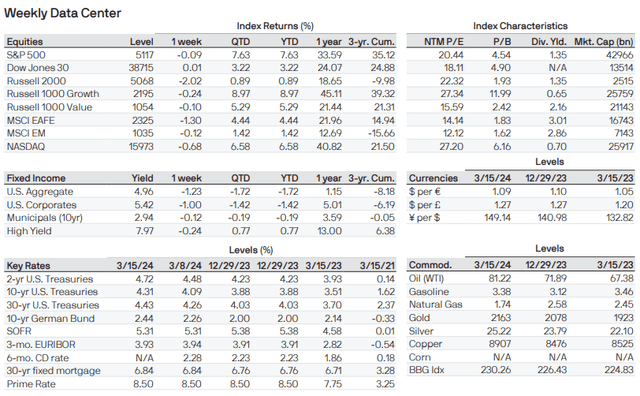

JPMorgan releases a nice Weekly Market Recap every week. These are the key index levels this week:

JPMorgan

Weekly performance roundup

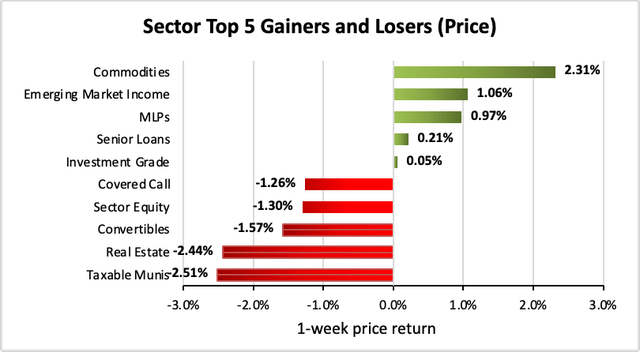

For CEFs, 5 out of 22 sectors were positive on price (down from 19 last week) and the average price return was -0.49% (down from +0.86 last week). The lead gainer was Commodities (+2.31%) while Taxable Munis lagged (-2.51%).

Income Lab

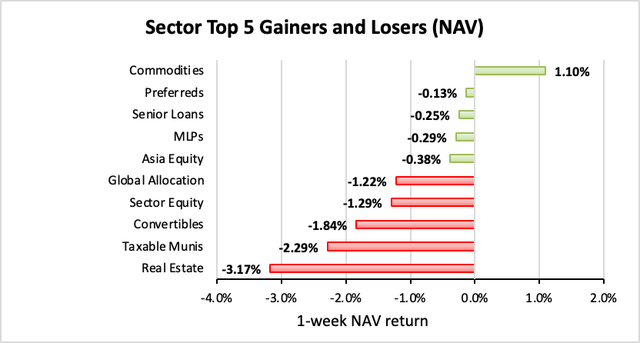

1 out of 22 sectors were positive on NAV (down from 22 last week), while the average NAV return was -0.79% (down from +1.49% last week). The top sector by NAV was Commodities (+1.10%) while the weakest sector by NAV was Real Estate (-3.17%).

Income Lab

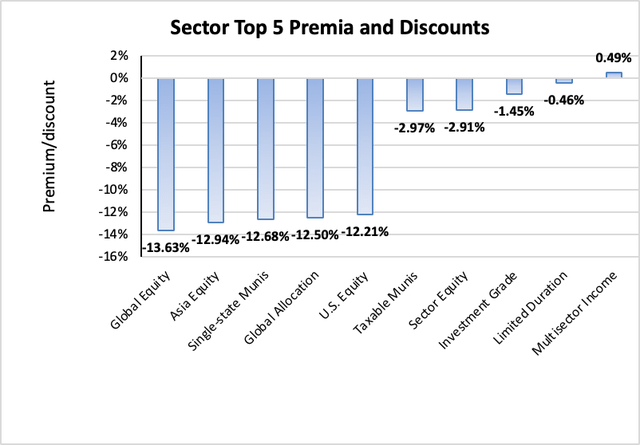

The sector with the highest premium was Multisector Income (+0.49%), while the sector with the widest discount is Global Equity (-13.63%). The average sector discount is -7.15% (up from -7.40% last week).

Income Lab

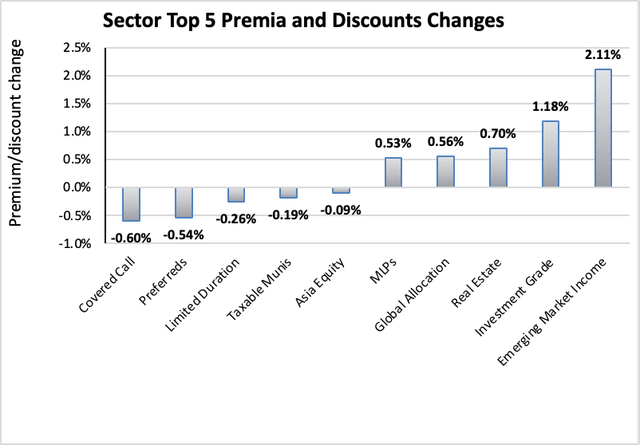

The sector with the highest premium/discount increase was Emerging Market Income (+2.11%), while Covered Call (-0.60%) showed the lowest premium/discount decline. The average change in premium/discount was +0.26% (up from +0.03% last week).

Income Lab

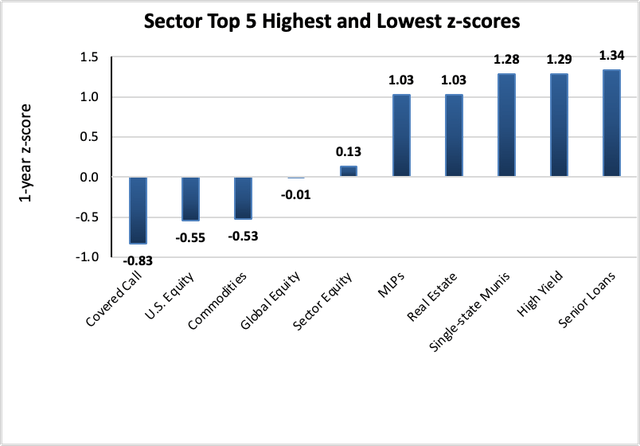

The sector with the highest average 1-year z-score is Senior Loans (+1.34), while the sector with the lowest average 1-year z-score is Covered Call (-0.83). The average z-score is +0.51 (up from +0.44 last week).

Income Lab

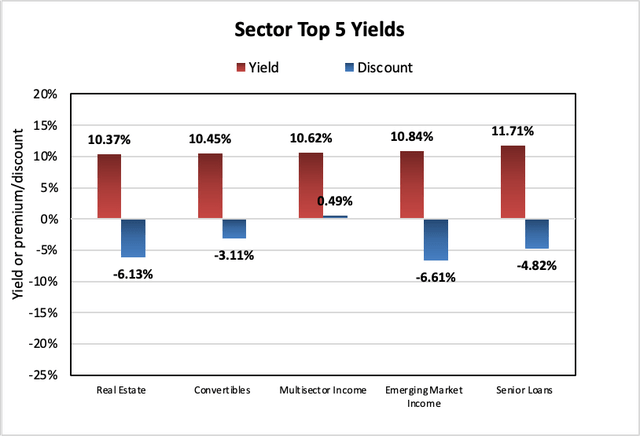

The sectors with the highest yields are Senior Loans (+11.71%), Emerging Market Income (+10.84%), and Multisector Income (+10.62%). Discounts are included for comparison. The average sector yield is +8.18% (up from +8.13% last week).

Income Lab

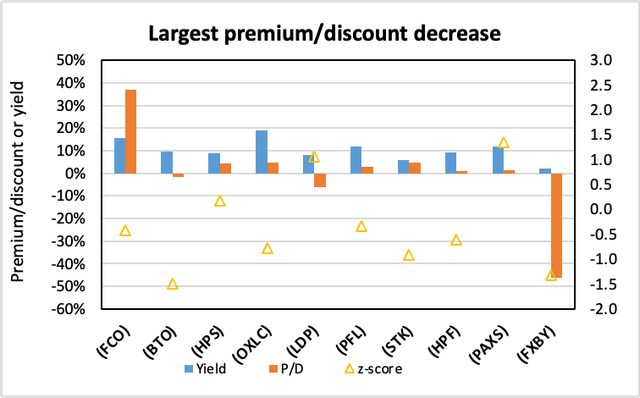

Individual CEFs that have undergone a significant decrease in premium/discount value over the past week, coupled optionally with an increasing NAV trend, a negative z-score, and/or are trading at a discount, are potential buy candidates.

| Fund | Ticker | P/D decrease | Yield | P/D | z-score | Price change | NAV change |

| abrdn Global Income Fund, Inc. | (FCO) | -3.97% | 15.64% | 36.99% | -0.4 | -3.07% | -0.25% |

| JHancock Financial Opportunities | (BTO) | -3.71% | 9.49% | -1.47% | -1.5 | -6.29% | -2.73% |

| JHancock Preferred Income III | (HPS) | -3.00% | 8.84% | 4.19% | 0.2 | -2.67% | 0.14% |

| Oxford Lane Capital Corp | (OXLC) | -2.58% | 18.97% | 4.57% | -0.8 | -2.13% | 0.00% |

| Cohen & Steers Ltd Duration Pref & Inc | (LDP) | -2.36% | 7.96% | -6.27% | 1.1 | -2.66% | -0.19% |

| PIMCO Income Strategy | (PFL) | -2.34% | 11.81% | 2.86% | -0.3 | -2.48% | -0.25% |

| Columbia Seligman Premium Technology Gr | (STK) | -2.29% | 5.87% | 4.89% | -0.9 | -3.58% | -1.44% |

| JHancock Preferred Income II | (HPF) | -2.12% | 9.20% | 1.07% | -0.6 | -1.95% | 0.13% |

| PIMCO Access Income | (PAXS) | -2.11% | 11.71% | 1.32% | 1.4 | -1.86% | 0.07% |

| FOXBY CORP | (OTCPK:FXBY) | -2.09% | 1.99% | -46.26% | -1.3 | -1.36% | 2.51% |

Income Lab

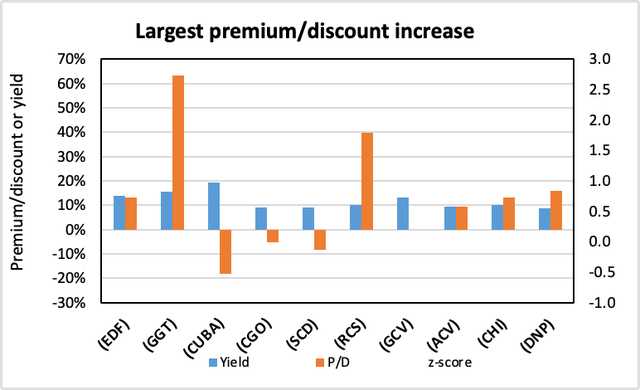

Conversely, individual CEFs that have undergone a significant increase in premium/discount value in the past week, coupled optionally with a decreasing NAV trend, a positive z-score, and/or are trading at a premium, are potential sell candidates.

| Fund | Ticker | P/D increase | Yield | P/D | z-score | Price change | NAV change |

| Virtus Stone Harbor Emerging Markets Inc | (EDF) | 8.61% | 13.93% | 13.13% | 2.0 | 5.94% | -1.51% |

| Gabelli Multimedia | (GGT) | 5.56% | 15.63% | 63.19% | 1.0 | -4.25% | -7.51% |

| Herzfeld Caribbean Basin | (CUBA) | 4.41% | 19.20% | -18.16% | 0.7 | 2.92% | -0.86% |

| Calamos Global Total Return | (CGO) | 4.01% | 9.14% | -5.23% | 2.0 | 3.19% | -1.16% |

| LMP Capital and Income | (SCD) | 3.56% | 9.19% | -8.21% | 2.7 | 1.10% | -1.22% |

| PIMCO Strategic Income Fund | (RCS) | 3.56% | 9.98% | 39.69% | 1.4 | 2.38% | -0.23% |

| Gabelli Conv Inc Secs | (GCV) | 3.42% | 13.15% | 0.00% | 0.2 | -1.35% | -3.95% |

| Virtus Diversified Inc & Conv Fund | (ACV) | 3.42% | 9.25% | 9.57% | 2.7 | 1.39% | -1.24% |

| Calamos Convertible Opp Inc | (CHI) | 3.23% | 10.11% | 13.03% | 1.7 | 0.80% | -2.06% |

| DNP Select Income | (DNP) | 2.94% | 8.69% | 15.83% | -0.6 | 1.24% | -1.32% |

Income Lab

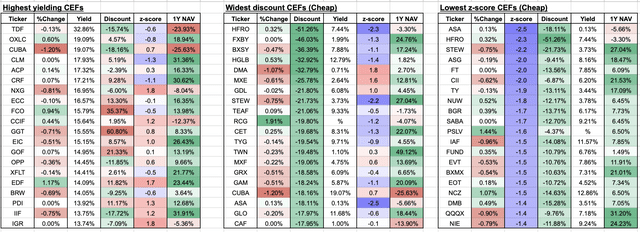

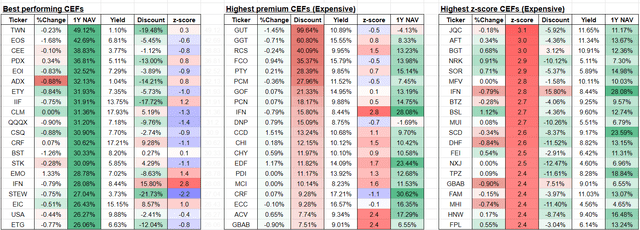

From our screener, here are the CEFs with the highest yields, widest discounts, and lowest 1-year z-scores:

Income Lab

From our screener, here are the CEFs with the best 1-year performance, highest premiums, and highest 1-year z-scores:

Income Lab

Recent corporate actions

These are from the past month. Any new news in the past week has a bolded date:

February 27, 2024 | Western Asset High Income Fund II Inc. Announces Preliminary Results of Transferable Rights Offering. Western Asset High Income Fund II Inc. (HIX) (“HIX” or the “Fund”) announced today the completion of its transferable rights offering (the “Offer”).

Upcoming corporate actions

These are from the past month. Any new news in the past week has a bolded date:

March 11, 2024 | Virtus Total Return Fund Inc. Announces Tender Offer Program. Virtus Total Return Fund Inc. (ZTR) (“the Fund”) today announced that its Board of Directors has approved a series of actions intended to enhance shareholder value, provide shareholders with an additional source of liquidity for their investment, and provide the potential to reduce the Fund’s trading discount to its net asset value per share (“NAV”) over time.

March 1, 2024 | First Trust Announces Shareholder Approvals of the Mergers. First Trust Advisors L.P. (“FTA”) announced today that shareholders of First Trust Energy Income and Growth Fund (FEN), First Trust MLP and Energy Income Fund (FEI), First Trust New Opportunities MLP & Energy Fund (FPL) and First Trust Energy Infrastructure Fund (FIF) (the “Target Funds” or each, individually, a “Target Fund”), each a closed-end management investment company managed by FTA and sub-advised by Energy Income Partners, LLC (“EIP”), approved the mergers of the Target Funds into FT Energy Income Partners Enhanced Income ETF (“EIPI”), a newly formed actively managed exchange-traded fund (“ETF”) that will be traded on the NYSE Arca and will be managed by FTA and sub-advised by EIP, at a joint special meeting of shareholders on February 29, 2024.

Recent activist or other CEF news

These are from the past month. Any new news in the past week has a bolded date:

March 1, 2024 | Pimco Dynamic Income Strategy Fund Declares Common Share Distributions. The Board of Trustees (the “Board”) of PIMCO Dynamic Income Strategy Fund (the “Fund”) (PDX)1 has declared the next two distributions for the Fund’s common shares, as summarized below.

Commentary

1. PDX’s distribution goes monthly (portfolio holding)

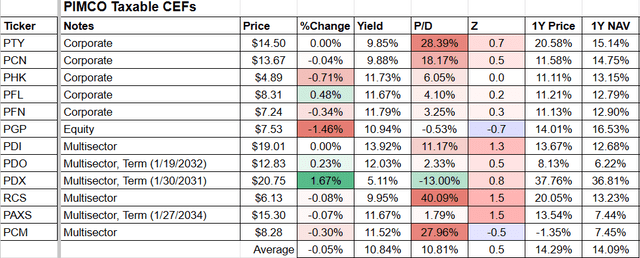

As we had anticipated, PIMCO moves to align PIMCO Dynamic Income Strategy Fund (PDX) more closely with the rest of its multisector income suite by moving to a monthly distribution schedule. As a reminder, PDX initially started as PIMCO Energy and Tactical Credit Opportunities Fund (NRGX), which was a fund that combined equity and fixed income investments with a focus on energy. However, on November 21, 2023, the fund’s investment strategy was modified to become a multisector income CEF that retained a minor energy tilt, and the fund was given a new name and ticker symbol. I suspect that the mandate change was likely an effort to ward off activist pressure from Saba Capital, who were building a significant stake in the CEF.

The March distribution will be the final quarterly distribution of $0.26 per share, which is itself a +18.2% increase from the prior quarterly distribution of $0.22. Starting from March, the fund intends to distribute monthly distributions at a level of $0.1133/month. This is equivalent to $0.34 per quarter, or a +30.7% increase from the March distribution, and a +54.5% increase from the previous December distribution.

At the April distribution level, the payout would still represent a conservative 5.78% NAV yield, which would be boosted to a 6.66% market yield due to the fund’s current -13.26% discount.

Despite the announcement, PDX still trades at a significantly wider discount than the peer group. I anticipate that as the change to the monthly distribution schedule becomes more well known, that there is room for PDX’s discount to narrow. Moreover, considering PDX’s strong NAV performance and lower yield in relation to its peers, there is likely additional room for its distribution to further increase which could provide an additional catalyst for discount narrowing.

From our CEF Watchlist:

Income Lab

However, it is worth pointing out that PDX’s portfolio remains predominantly in equity, indicating that there hasn’t been a significant shift in its holdings since it announced its transition to a credit fund in November. Hence, PDX’s performance going forward is still going to primarily reflect the performance of the stock markets rather than the bond markets. Unfortunately, the timeline for PIMCO’s complete transition of PDX into a multisector credit fund remains uncertain at this point.

PIMCO

We own PDX in both our Income Generator and Tactical Income-100 portfolios.

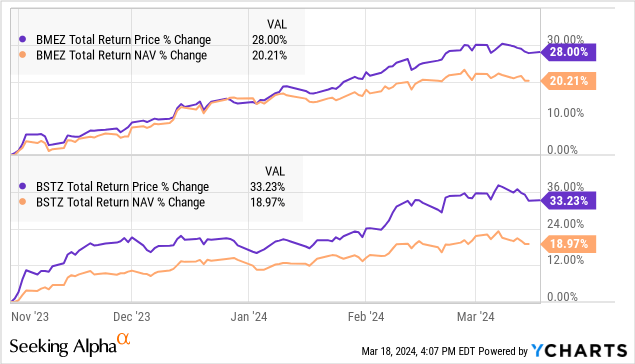

2. Saba targets BSTZ (portfolio holding)

The activists at Saba have been conducting a high-profile campaign against BlackRock CEFs and have been amassing very large stakes in these funds to push for shareholder friendly actions. These include a $252 million stake in BCAT, $398 million in BIGZ, $329 million in BMEZ and $462 million in ECAT.

Until recently however, the BlackRock Science and Technology Term Trust (BSTZ) was a conspicuous absentee from its target list. Well, not anymore!

On February 2, Saba filed its first 13D against BSTZ, which is needed to indicate active intent. The filing itself is rather boilerplate, and includes as usual Saba’s intent to make shareholder proposals and nominate allies to the board:

The Reporting Persons may also propose or take one or more of the actions described in subsections A through J of Item 4 of Schedule 13D, including the solicitation of proxies, and may discuss such actions with the Issuer and Issuer’s management and the board of directors, other stockholders of the Issuer and other interested parties. The Reporting Persons may make binding or non-binding shareholder proposals, or may nominate one or more individuals as nominees for election to the Board in connection with their investment in the Common Shares of the Issuer.

The latest filing shows that Saba owns 5.66 million, or 7.44% of BSTZ outstanding shares, representing a $104 million investment.

We own both BSTZ and BMEZ in our Tactical Income-100 portfolio, which have discounts of -12.02% and -15.29% respectively. Both funds have performed well since the lows of last October, with discounts narrowing significantly. I view Saba’s involvement as positive as this may stimulate the discount to contract further should Saba be able to force any concessions from the fund giant.

YCharts

We own BSTZ in our Tactical Income-100 portfolio.

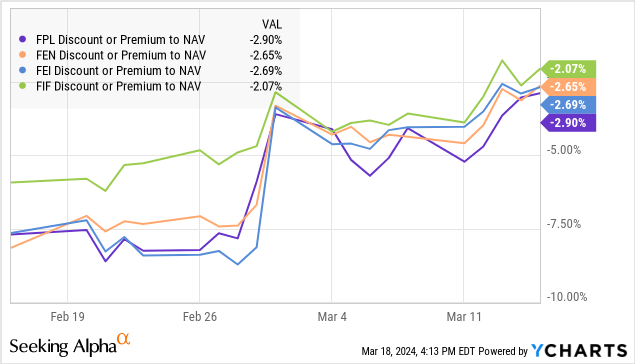

3. First Trust MLP CEF mergers approved (portfolio holding)

As discussed in a previous CEF Weekly Roundup, First Trust had been proposing to merge their MLP CEFs, namely First Trust Energy Income and Growth Fund (FEN), First Trust MLP and Energy Income Fund (FEI), First Trust New Opportunities MLP & Energy Fund (FPL) and First Trust Energy Infrastructure Fund (FIF) into a newly created ETF, the First Trust Energy Income Partners Enhanced Income ETF.

The mergers have now been approved by the stockholders of all four CEFs, and the consolidation is slated to take place “by the end of April 2024”. A positive outcome was expected as conversion into an ETF structure would eliminate the discounts of the CEFs, since ETFs always trade near NAV. As we wrote last November:

I do expect the votes to go through because shareholders will benefit from being able to exit at NAV. With FEI and FIF still at -8.50% and -6.29% discounts respectively, we’re content to hold onto these funds in our Tactical Income-100 portfolio and continue to harvest the alpha that would come from discount contraction as the merger date nears.

The discounts tightened further upon announcement that the mergers were approved by shareholders.

YCharts

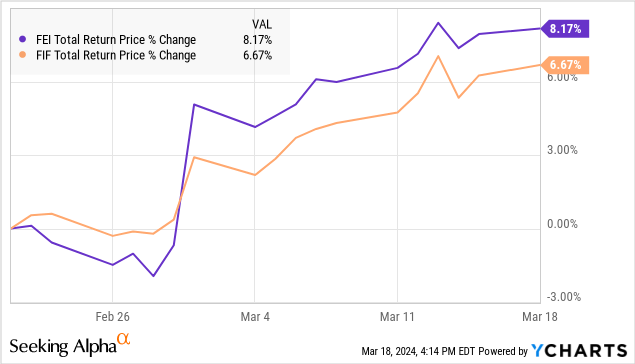

We had recently switched from FEI to add to FIF in our Tactical Income-100 portfolio because we were worried about the potential NAV impact that could affect FEI. As a reminder, FEI, like its close sister funds FPL and FEN, are structured as C-corps in order to allow them to hold over 25% of MLPs. As a result, this means that they are subject to taxation at the fund level. In contrast, FIF is structured as a RIC, which is the typical structure for most other CEFs, and is not subject to taxation at the fund level. However, RIC cannot hold more than 25% of MLPs.

The proxy statement outlining the merger had indicated that the C-Corps could potentially suffer a negative NAV impact as a result of having to deem its assets as having been sold at fair value due to the transition to the ETF, leading to a possible tax hit.

However, this fear did not come to pass as we now know that tax implications are likely to be minimal. In the press release announcing the shareholder approval for the mergers, First Trust indicated that FEI and FPL would be subject to NAV adjustments of approximately +$0.030 and -$0.083 respectively, while FEN would be unaffected.

As a result, our switch from FEI to FIF was unnecessary and caused 1.5% of gains to be left on the table. Nevertheless, a profit is a profit!

YCharts

We own FIF in our Tactical Income-100 portfolio.

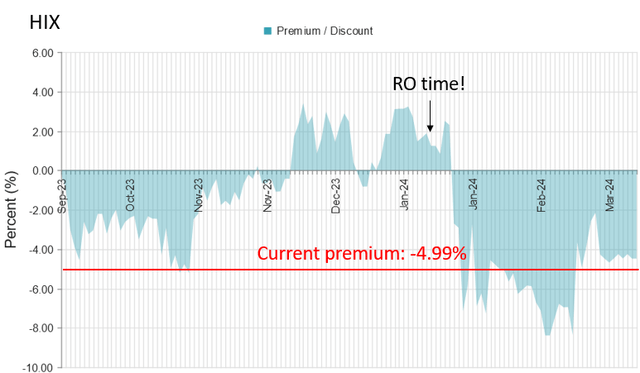

4. HIX rights offering results

Rights offerings have not been very common last year due to the wide discounts in CEFs. This is because rights offerings are typically dilutive, and having to dilute shareholders when the fund is already trading at a deep discount generally leaves a poor taste in investors’ mouths.

CEF discounts did recover towards the end of last year, and apparently the managers of Western Asset High Income Fund II Inc. (HIX) couldn’t wait to pull the trigger when HIX’s valuation poked into slight premium territory. Predictably, the announcement of the offering triggered an immediate devaluation of the shares which reliably dropped into discount territory over the course of the offering.

CEFConnect

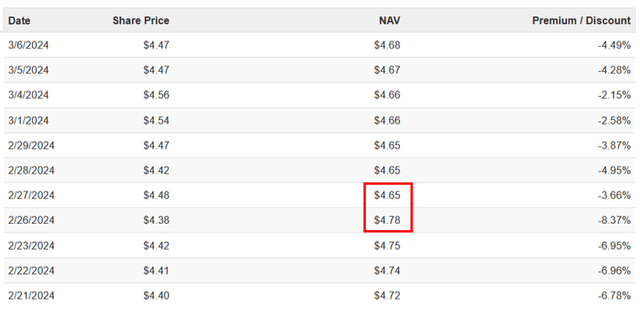

The subscription price was the greater of 92.5% of market price of 90% of NAV. The NAV floor was hit, meaning that the new shares were issued at $4.30, a -10% discount to the NAV on expiry date. Because HIX’s discount was narrower than -10% at expiry, it was beneficial for investors to subscribe. Indeed, this offering was oversubscribed, allowing the fund to increase its share count by the maximum limit of +33.3%. However, the issuance of new shares below NAV also resulted in a NAV decrease of -$0.12 per share or -2.5%, which was reflected the following day. Simultaneously, the discount immediately adjusted from -8.37% to -3.66%.

CEFConnect

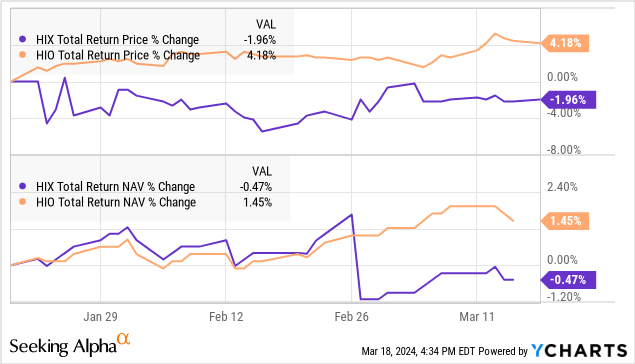

Our recommended “sell and rebuy” strategy would have worked again. For example switching from HIX to the peer fund Western Asset High Income Opportunity Fund Inc. (HIO) over the course of the offering would have generated around +6% alpha (or “free shares” if one conducts a HIX –> HIO –> HIX rotation trade), outweighing the minor benefits of subscribing for new shares at a slight discount.

YCharts

Read the full article here

")

")