")

")

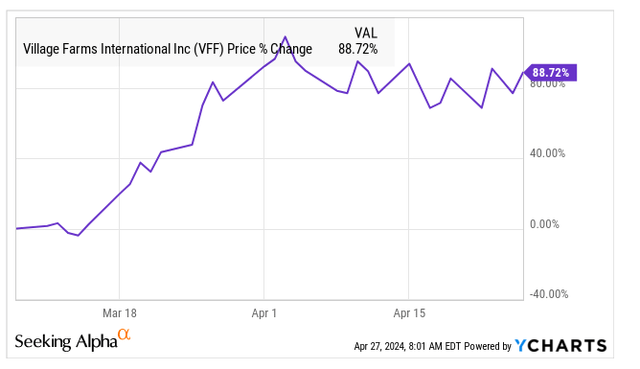

I exited Village Farms (NASDAQ:VFF) in my model portfolio for subscribers of my investment group yesterday. I last wrote it up here just ahead of their Q4 report and discussed the extremely low valuation. The stock has soared since then:

YCharts

I had a Strong Buy rating on it then, and I am downgrading it to Neutral today. I think that the stock is still cheap, but in this follow up I explain why I am Neutral for now.

The Village Farms Q4 Report

Village Farms had been expected by analysts, according to Sentieo, to generate revenue of $70 million in Q4 with adjusted EBITDA of $3 million. The company reported total revenue of $74.2 million, a 7% gain that was above expectations. Adjusted EBITDA, though, was below expectations at -$0.7 million. This was much better than the loss of $11.7 million a year earlier.

The business that I really like, its Canadian cannabis operations, saw revenue grow 15% to $32 million. Adjusted EBITDA in that unit was $1.5 million, a decline from the $6.4 million a year earlier. Village Farms Fresh, its large produce unit, saw revenue expand slightly to $37.1 million. Its adjusted EBITDA improved from -$3.0 million to -$0.6 million. The U.S. Cannabis unit, which is CBD from the former Balanced Health Botanicals that it acquired, saw revenue decline slightly to $5.1 million with adjusted EBITDA improving to $0.3 million.

Cash flow from operations was -$1.5 million during Q4 after a hugely positive Q3 at $12.1 million. For the year, cash flow from operations was $5.3 million, which was a lot better than the use of $19.9 million in 2022. Capital expenditures fell a lot in 2023, but they were slightly above the cash flow from operations.

Cash fell slightly in Q4 to $30.3 million. Total debt was reported at $52 million, leaving net debt of $22.3 million, up sequentially from $17.6 million. The current ratio is healthy at 2.1X. Tangible equity fell to $214.4 million from $219.4 million at the end of Q3 and up from the $199.7 million at the end of 2022 (thanks to the equity raise in early 2023).

The Village Farms Outlook Has Declined Modestly

Ahead of the Q4 report, analysts were expecting total revenue in 2024 to be $300 million and then to grow in 2025 to $337 million. Their outlook for adjusted EBITDA in 2024 was $12 million and then $23 million in 2025.

Now, the analysts are projecting for 2024 that revenue will increase 8% to $308 million, which is a bit higher than their prior forecast. They continue to predict that adjusted EBITDA will be $12 million, up 54%.

The outlook for 2025 is that revenue will be a little less than they had expected. Their forecast is now $335 million, up 9%. The analysts have also reduced their adjusted EBITDA forecast to $19 million, up 60%. This margin of 5.6% would exceed the 2021 margin of 5.2%.

Village Farms Still Trades Below Tangible Book Value

I was previously most focused on the very low price-to-tangible book value ratio. In that Strong Buy report ahead of the Q4 financials, I reported that it was just 36%, which was insanely low. With the slightly lower tangible book value and the rocketing price, it is now 71%. My target in that March report was 75%, so the stock is close to the full valuation that I had predicted.

Comparing a stock to its tangible book value is helpful for assessing potential downside risk, but looking at the valuation relative to earnings is more helpful. In that last report, the enterprise value was just 8.5X projected 2024 adjusted EBITDA. Now, the enterprise value, which is boosted by the slightly higher net debt and the soaring stock price is $177 million, which is 14.8X the 2024 projected adjusted EBITDA and just 9.3X projected adjusted EBITDA for 2025.

I am raising my target for the end of 2024 from 75% of tangible book value to 90%. This works out to $1.70 (26% higher), but it doesn’t include the exercise of the $1.65 warrants that are below tangible book value. This price would work out to a market cap of $193 million and an enterprise value of $215 million, which would be about 11.3X projected adjusted EBITDA for 2025.

The Village Farms Chart No Longer Says Buy

What a great year for Village Farms! The stock has almost tripled from the lows set in Q3:

Schwab

While the past year has been great, a longer look shows how weak the stock has been:

Schwab

The stock, while it is up a lot from the bottom, is down 93% from its peak in early 2021. My own view of the chart is that it should find support just below $1. I see resistance at $1.50 and note that there are 18.4 million warrants at $1.65.

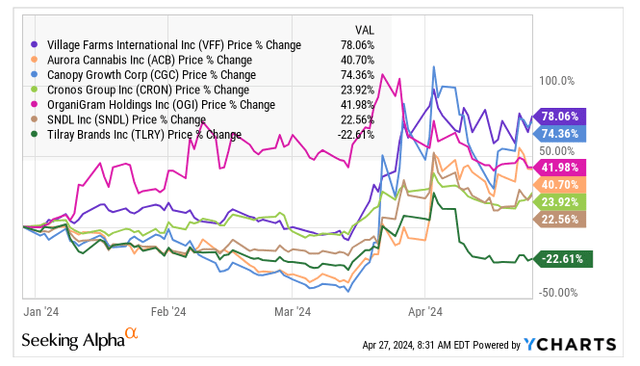

So far in 2024, Village Farms is up 78%. This compares favorably to the six cannabis stocks that are in the New Cannabis Ventures Global Cannabis Stock Index:

YCharts

I wrote last week about how much I like Organigram (OGI), the only LP I own in my model portfolio right now after exiting the other two that I like, Village Farms and Cronos Group (CRON). Organigram is not only my favorite Canadian LP, it is my favorite cannabis stock.

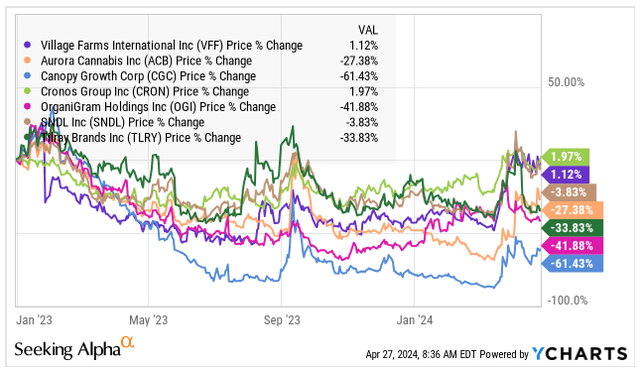

Taking a look since the end of 2022, Village Farms is one of two stocks that have increased in value:

YCharts

Conclusion

Just because a stock goes up a lot does not mean that one should sell it. I feel very fortunate that the stock finally filled that gap left behind in early 2023 when the company surprised the market with a capital raise. I am happy that I stuck with it in my model portfolio and just kept buying the new lows. I exited the name for the first time in over a year despite my view that the company is doing a very good job in the Canadian cannabis market.

My exit isn’t because I don’t like their CBD business or their produce business. I have called these out in my prior articles! I find the stock cheap to its tangible book value, and I am open to the possibility of a strategic buyer showing up, but I am not holding my breath. For now, the delisting risk has faded, but if it were to fall below $1 again, this risk would come back.

So, why am I exiting a stock that still seems cheap? As I discussed above, the chart is no longer compelling me to want to own it. I am highly concerned that Canopy Growth and Tilray could fall in price, and this could weigh upon the stocks of other LPs, like Village Farms. I am also concerned that cannabis stocks overall could come under pressure. The stock is not in the New Cannabis Ventures Global Cannabis Stock Index that I am trying to outperform.

For those that are truly long-term investors, there is no reason to sell this stock in my view. I am hoping for another opportunity to buy it back. For now, I prefer Organigram, which is a pure-play and which is trading at 89% of tangible book value with a big strategic investor that is investing more at a price above the current price.

Read the full article here

")

")

")

")

")