or Bonk (BONK)")

ZIM Integrated Shipping Services Ltd. (NYSE:ZIM) is an Israeli global container liner shipping company greatly benefited by Red Sea disruption.

Background

I have covered ZIM previously, investors should view this as an update to the previous article on the company, where I did an extensive Business Overview and explained the investment thesis in detail.

Since the publication of the previous article, the company has reported Q4 2023 results and provided 2024 guidance. In the following sections, I will provide commentary on these developments and incorporate the updated information into the valuation analysis.

Meanwhile, the Red Sea situation has not improved, and rates have remained elevated but softening. While I initially anticipated a potential uptick post-Chinese New Year due to strong US demand, this assumption has proven wrong. Rates have fallen quicker than what I was expecting and just this week there are some early signs of stabilization with FBX, freight futures and liners increasing rates. It’s important to remember that this time of the year is typically the low season, with stronger rates starting in April through to H2.

Given the lower rates than my previous expectations and the market’s reluctance to consider the Red Sea disruptions as a new normal, I am revising the fair value from $30 per share, as stated in the previous article, to a range of $20-25 per share. I believe this adjustment reflects a more realistic assessment, considering the current circumstances. Moreover, there is potential for further improvement in the fair value if rates demonstrate resilience over time.

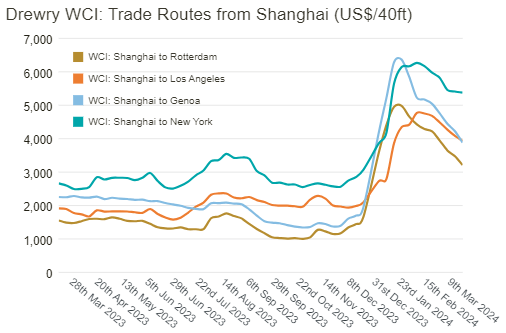

Drewry Index (Drewry)

Regarding the Gaza situation, there has been no ceasefire and it seems that the Rafah offensive is imminent. In the event of such an offensive, prospects for a ceasefire appear bleak, prolonging the conflict for several more months. Additionally, the situation in the Lebanese border is escalating quickly and could start another front. As long as these conflicts persist, Houthis will continue targeting Western ships in the Red Sea area.

Another noteworthy development to keep in mind is the kick-off of Transpacific contract talks. Xeneta expects these negotiations might be difficult, but thanks to the strong rates, shipping companies should still lock in favorable deals. While ZIM only aims to fix about 50% of their transpacific volume, these negotiations set the vibe for the rest of the year.

Guidance & Conference Calls comments

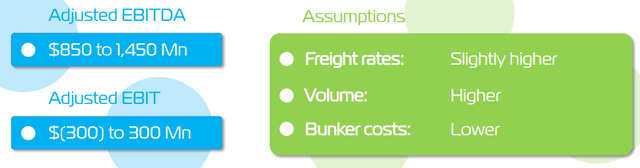

Management provided a muted guidance with an Adjusted EBITDA ranging from $850 to $1450 million, and adjusted EBIT between -$300 million to $300 million. Even in the upper band, it suggests minimal profit, since in 2023 Financial Expenses were $305 million.

Market reaction demonstrated that investors were expecting a better outlook.

Guidance (ZIM Q4 presentation)

The guidance provided is really conservative, assuming a short-term resolution of the Red Sea disruption at the lower end and a resolution by Q3 at the upper end. Management expects a quick rate decline to unprofitable levels around November/December 2023 following the resumption of Red Sea transits.

While I agree with the company’s assumption of rapid rate decline once Red Sea becomes navigable again, I expect the resolution to take longer than the company anticipates. Consequently, I believe management will do an important guidance revision by Q2. Despite knowing the rates fixed in the Transpacific contract negotiations by the Q1 release, I don’t expect a substantial revision in guidance because management could still anticipate a resumption of the Suez Canal transit by Q3. However, if the disruption in the Red Sea persists by the Q2 earnings release, there should be a significant upward revision in guidance.

An important point from the guidance is the expected higher volume. During the conference call, management commented that it expects over 10% increase in volume, along with a reduction in bunker costs. These two factors are expected to significantly lower the cost per TEU.

Another notable comment from the conference call is that the dividend policy stands. ZIM dividend policy is as follows: “the Company intends to distribute 30-50% of annual net income as a dividend to shareholders.” Despite expecting a positive EPS in Q1 I do not anticipate a dividend. At the midpoint of the guidance, the net income for the entire year is projected to be negative. In order to pay a dividend in Q1 they should do a meaningful increase in the guidance. However, as commented before, I do anticipate an important guidance revision by Q2 results that will warrant a dividend.

Finally, there were interesting comments regarding the supply and demand balance. Management estimates that longer voyages around the Cape have absorbed approximately 6% to 7% of global capacity. At the same time US demand is really strong and global trade is expected to grow between 3 or 4%. Taken together, these factors increase demand by around 10% compared to December levels.

On the supply side, management expects about 10% of current global capacity to be delivered during the year and a 2% scrapping, resulting in an overall 8%increase in supply.

In the event that Red Sea disruption last all year, the increased demand is expected to outpace supply by 2%. This suggests that rates in December 2024 should exceed those of December 2023, despite the year seeing the highest delivery capacity in history.

Financial Position & Stock Valuation

Financial Position (ZIM Q4 presentation)

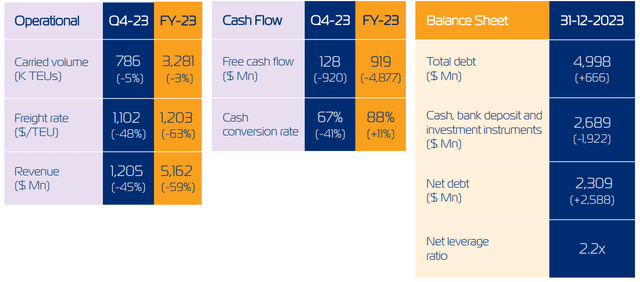

In Q4, ZIM reported revenue of $1.21 billion and EPS of -$1.23, in line with estimations. The main negative was the reduction in carried volume from 867k TEU in Q3-23 to 786k TEU in Q4-24. Management attributed this to a one-off occurrence mainly due to Cape of Good Hope diversion and anticipated volumes to rebound by over 10% compared to FY-23 volumes.

Another important factor is the remaining cash per share. In the previous article, I estimated a cash burn of $300 million and expected year-end cash above $23 per share. However, due to lower volumes and revenues, the cash burn amounted to $423 million, resulting in a Q4-23 cash per share of $22.4.

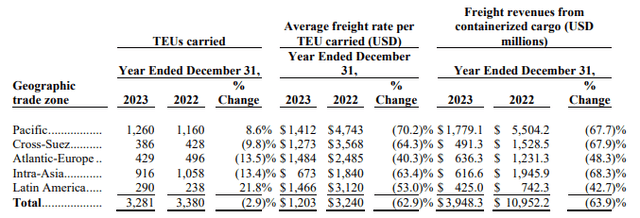

In the Annual Report, ZIM provided a useful table to better estimate future earnings potential:

ZIM Annual Report

The Pacific region stands out as the most significant area, with a 45% of the total freight revenues and one of the highest freights per TEU. During 2024 the volume in this Pacific zone will continue to increase until all newbuild capacity is delivered. In contrast, Intra-Asia experiences lower rates due to the use of smaller ships and its focus on regional trade. Management commented that moved some capacity from Intra-Asia to Latin America to improve profitability, indicating strategic efforts to boost financial performance.

This segmentation is very important because, as shown in the Drewry chart in the background section, Pacific routes (Shanghai to Los Angeles, and to a lesser extent, Shanghai to New York) witnessed the most significant increases.

Considering this information alongside management’s comments, it is possible to estimate earnings and cash evolution beyond the provided guidance, which I consider highly conservative. My estimation is for a realized rates around $1.600/TEU in the first quarter, around current SCFI levels for the second and third quarter, $1.750/TEU, and a decline to $1.350/TEU in Q4. Based on management’s comments, I expect they will carry 3.6 million TEU, $129 million CAPEX due to vessels purchases and a small reduction in debt service to $2 billion as they plan to redeliver the 30 additional vessels up for renewal to compensate the newbuilds. These projections, excluding working capital movements and taxes, suggest an approximately $10 EPS and a $5 dividend for 2024.

I consider these assumptions realistic if Red Sea disruption persists and even conservative depending on the rates achieved during ongoing contract negotiations.

Net Income and Cash Projections (Author)

With this comparison, it is easy to see the difference between an immediate stop of Houthis attacks (low end of the guidance) and a prolonged disruption. I consider the low end of the guidance as a worst-case scenario, but even under these conditions, ZIM will end the year with more than $10 cash per share and tangible assets exceeding $7 (calculation provided below). Right now, the stock is under $10 per share. In such a scenario, scrapping will be higher than expected and will help rebalance the market. ZIM will be strategically positioned with reduced operating expenses in 2025 and the flexibility to redeliver 37 additional ships during the year if rates aren’t profitable.

In a more realistic scenario where the Red Sea disruption last longer, ZIM could end the year generating $10 EPS and with $27 in cash per share by year-end, before distributing a $5 dividend. There is potential for further upside if rates are stronger than expected or contract negotiations achieve around current rates. With Q1 results there will be more clarity for the whole year. My expectations for Q1 are around $2.5 EPS with no dividend, and a slight cash reduction due to the vessels purchases. For Q2 and Q3, I anticipate above $7 EPS for both quarters and dividend over $2 in total. In Q4, I expect less than $1 EPS with a slight cash burn but a $3 EPS catch-up dividend.

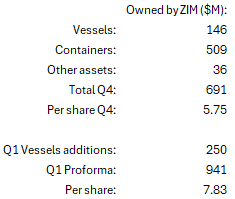

Finally, during the results presentation, management disclosed that in February ZIM exercised a purchase option of five vessels for a consideration of $129 million. In the previous article, I already calculated the value of ZIM’s assets with a result above $5 per share. These recent acquired vessels have a market value around $250 million, increasing the assets owned by the company to over $7 per share.

Asset’s Value (Author)

In summary, 2024 is a transition year for ZIM as it receives all the efficient newbuilds while reducing the expensive covid era time charters through the redelivery of 30 ships during 2024 and 37 more during 2025. This will set ZIM as one of the most cost-effective liners for years to come. To a great extent the value of ZIM will depend on how it finishes this transition in 2024 and starts 2025. Before the Red Sea disruption, 2024 was expected to consume all the cash amassed during the covid boom, which led ZIM to trade just above $6 despite having over $20 cash per share. However, the Houthis attacks changed the outlook, potentially turning ZIM’s transition year into a highly profitable one. In the unlikely event of an imminent resolution, ZIM will hold $12 per share in cash by the end of 2024. In the more realistic scenario of a prolonged disruption, ZIM could generate above $10 EPS during 2024, end the year with more than $27 cash per share and distribute $5 in dividends. In this scenario 2025 will have lower rates due to limited scrapping and continued deliveries, however, ZIM will be in a much better position, with lower costs and more cash that at the start of 2024.

Considering all these factors, the value of owned assets and the uncertainties surrounding future rates, my fair value estimate is $25 per share. However, applying an extra discount due to market reluctance and setting the fair value at $20 per share, still implies an upside of over 100%.

Risk

The risks remain the same as in the previous article. Once the Suez Canal becomes safe for transit again, a process that might take months or even years, rates will drop quickly to levels that could lead to losses until the oversupply is tackled through scrapping. Given the huge orderbook and the focus on emissions reduction, I expect a significant uptick in scrapping once rates return to normal, as there are a lot of scrapping candidates in the vintage fleet.

Conclusion

In conclusion, increased rates and ZIM’s solid financial position will allow a smooth transition to lower operational expenses with the arrival of newbuilds and redelivery of expensive covid chartered vessels.

The Red Sea disruption has transformed ZIM outlook from a heavy 2024 cash burn year to a profitable year, with the potential to finish the year above $27 cash per share and arriving at 2025 with an improved market position.

Even in the unlikely event of an immediate resumption of Suez Canal transits, ZIM will end the year with a comfortable cash position. Furthermore, with each passing day without a resolution and current rates, the cash cushion continues to grow.

My expectation is that the resolution will take longer than expected, and that the market will realize the earnings potential, at the very latest, with Q2 results. With this framework and being conservative I set the fair value at $20 per share, offering more than 100% upside.

Read the full article here

(NASDAQ:GOOG)")

")